SME owners often face the challenge of adapting business strategy to a highly dynamic environment while simultaneously managing day-to-day financial operations. It's like Formula 1 racers, where only precise and quick decisions can save them from

failure. But how exactly can SME banking services help business owners? Find out how a customer-centric approach can be used to design the next-gen SME banking.

SMEs Lack More Value from Banking Providers

Small entrepreneurs face fragmented financial management experience because they need to use several services to cover all their daily business needs. It emphasizes the need for more than basic account services and the fact that banks don't satisfy all their

service needs. SMEs are looking for support and guidance on managing finances, understanding where to focus attention and interpreting KPIs. They often lack financial experience and need a simple, clear connection between financial data and the business to

make the best decisions for the future.

Recent EY research reveals that only 18% of SMEs and self-employed individuals feel they are understood by their banks and have strong relationships with their banking providers, while others expect financial institutions to have a stronger knowledge of

their business industry and initiate proactive communication.

However, banks hold a powerful resource: the financial data of SMEs they gather with their consent. Leveraging this data, banks can offer customer-centric and tailored SME banking solutions, including cash flow analysis and fund allocation guidance, aligning

with customer expectations.

Additionally, the EY report reveals that 82% of SMEs actively endorse data sharing, driven by a desire for enhanced services and tailored financial advice to fuel their business development efforts. Furthermore, armed with data from SMEs spanning diverse

industries, banks have the potential to facilitate connections among like-minded and complementary clients, fostering the growth of their businesses. A significant portion of SMEs (81%) would find the offer of tailored networking opportunities very valuable

for their business and would use it.

“The bank is helpful with daily things like account administration and even troubleshooting, but they don’t come up with new ideas or technology,” Barbara Fretter and Maarten Lammens, owners of Solids Development Consult.

Which Digital Banking Services do SMEs desire?

Financial institutions can provide SMEs with a range of valuable digital services using innovative technologies and next-gen user experience design:

1. AI-powered personal finance advisors

More and more banks integrate AI into their operations, potentially limiting SMEs' dissatisfaction points. An EY analysis of over 5,000 SMEs worldwide reveals striking frustration levels: 69% of SMEs express dissatisfaction about lacking the proactive communication

regarding their businesses from the bank's side, and 76% lack confidence in how banks understand their industry.

AI emerges as a powerful ally for banks and SMEs in addressing these issues. It enhances proactive communication by keeping SMEs informed with industry updates, preserving banks' human resources for advanced SME business growth consultations. AI-powered

personal finance advisors also enable banks to offer predictive cash flow insights, optimizing resource allocation and fostering business growth.

Additionally, AI aids in categorizing and tracking business expenses and identifying areas for cost-cutting or optimization. With limited time and the absence of finance education, AI can step in and educate business owners about financial management essentials

and answer complex questions in a straightforward, simple and focused way to help business owners save time.

2. All-in-one platform

As super apps for individuals become commonplace, the question arises: what about the needs for SMEs? Envision a landscape in which banks seamlessly integrate the most valuable platforms and tools for SMEs, such as SaaS solutions Xero, Sage, Quickbooks,

Debitoor or Lexware. These platforms already serve as the primary financial interface to enhance the SMEs’ banking UX, consolidating bank accounts, transactions and accounts payable and receivable.

By integrating different financial services and other financial management tools, banks could completely change the financial management habits of SMEs, resulting in a significant boost in customer base and loyalty as they would fulfill all of the SMEs'

banking requirements in one place.

This transformation can turn banks' digital solutions into comprehensive ecosystems regardless of the device or platform they choose. As a result, SMEs would receive a smooth and seamless user experience, eliminating the complexity of using multiple financial

platforms and tools.

In EY's research on SMEs' digital expectations, 56% of respondents expressed their desire for a single integrated platform for financial management, consolidating financial products from multiple banks and financial providers. It is worth mentioning that

banks are the ones SMEs expect to provide these integrations: 22% of research respondents would prefer accessing this through a bank, while 17% of SMEs are open to paying additional fees for such a service.

3. Digital experience and contextual personalization

It is worth mentioning that business owners have high expectations when it comes to SME banking UX, which is continuously influenced by advancements in digital interactions with other banks, financial providers and digital experiences from other industries.

Ernst & Young's research on SME banking transformation highlights SMEs' strong demand for a seamless digital experience from their financial service providers, with 53% viewing it as crucial for business development. Additionally, 68% of SMEs aim to digitally

manage various aspects of their business, including financial management.

Today, we witness the blurred boundaries between experiences with products from various industries. The McKinsey's report illustrates a growing consumer desire for cross-sector, real-time, personalized and convenient services. People desire uniform and seamless

experiences, whether they're watching suggested movies on Netflix, getting notifications on their iPhones or acquiring offered products in a mobile banking app.

Therefore, banks should explore transferring their digital capabilities and the lessons they have gleaned from retail banking to SME banking. Banks can extend personalized notifications that keep businesses informed about critical changes in their operations

or account balances.

Furthermore, by having all the financial data of SMEs, banks can gain a comprehensive understanding of the customer's financial needs, offer tailored solutions and, in some cases, proactively prevent threats by informing business owners about unusual transactions.

Through a personalized approach, banks can enhance customer loyalty by making SMEs feel valued and confident in the bank's proficiency in serving businesses within a specific industry.

4. Customer care

Customer care is a cornerstone of enhancing SME customer loyalty and satisfaction with financial service providers. Recent data from a McKinsey survey of German SMEs highlights 36% of respondents citing excellent customer service as their top reason for

choosing their primary bank. Emphasizing the fundamentals is essential, as 75% of SMEs from the same survey look for responsiveness, speedy service and streamlined processes from their bank or financial services provider. This supports the banks' need to integrate

a customer-centric mindset while serving businesses.

In light of evolving global conditions and external influences, SMEs now, more than ever, seek financial guidance and support to sustain profitability. Leveraging decades of experience navigating various crises and instabilities, traditional banks are well-positioned

to share invaluable insights and expertise with their customers.

EY's research reveals challenges, such as 22% needing help accessing financial advice and 21% seeking general business management support from their bank. This data underscores the need for banks to reevaluate their customer care strategies to meet SMEs'

banking needs, thereby ensuring they remain competitive in the market.

Of course, there are already great banks on the market that successfully serve SMEs' needs. For example, the OCBC Bank business banking app is a personal assistant for small and medium enterprises. The bank's integrated tools allow SMEs to access a 360-degree

view of their sales, expenses and cash flow trends to better understand their business and make reasonable and strategic business decisions. Businesses can also receive an expense analysis of spending to control costs and manage changing expenses needs effectively.

Design: Simplicity and full control for higher efficiency

We aimed to simplify financial management for those who drive their own business and were inspired by consistent user experiences provided by giants like McDonald's and Apple.

McDonald's ensures consistent quality in every location by simplifying processes and building operational excellence. At the same time, Apple is a master of combining several products into one solution, becoming a leader in technology.

SME banking design should prioritize simplicity, aiming to eliminate chaos and stress associated with business financial management. Acting as a trusted guide, it should easily and quickly provide users with the information they need, while instilling positive

emotions, such as trust, calm and inspiration.

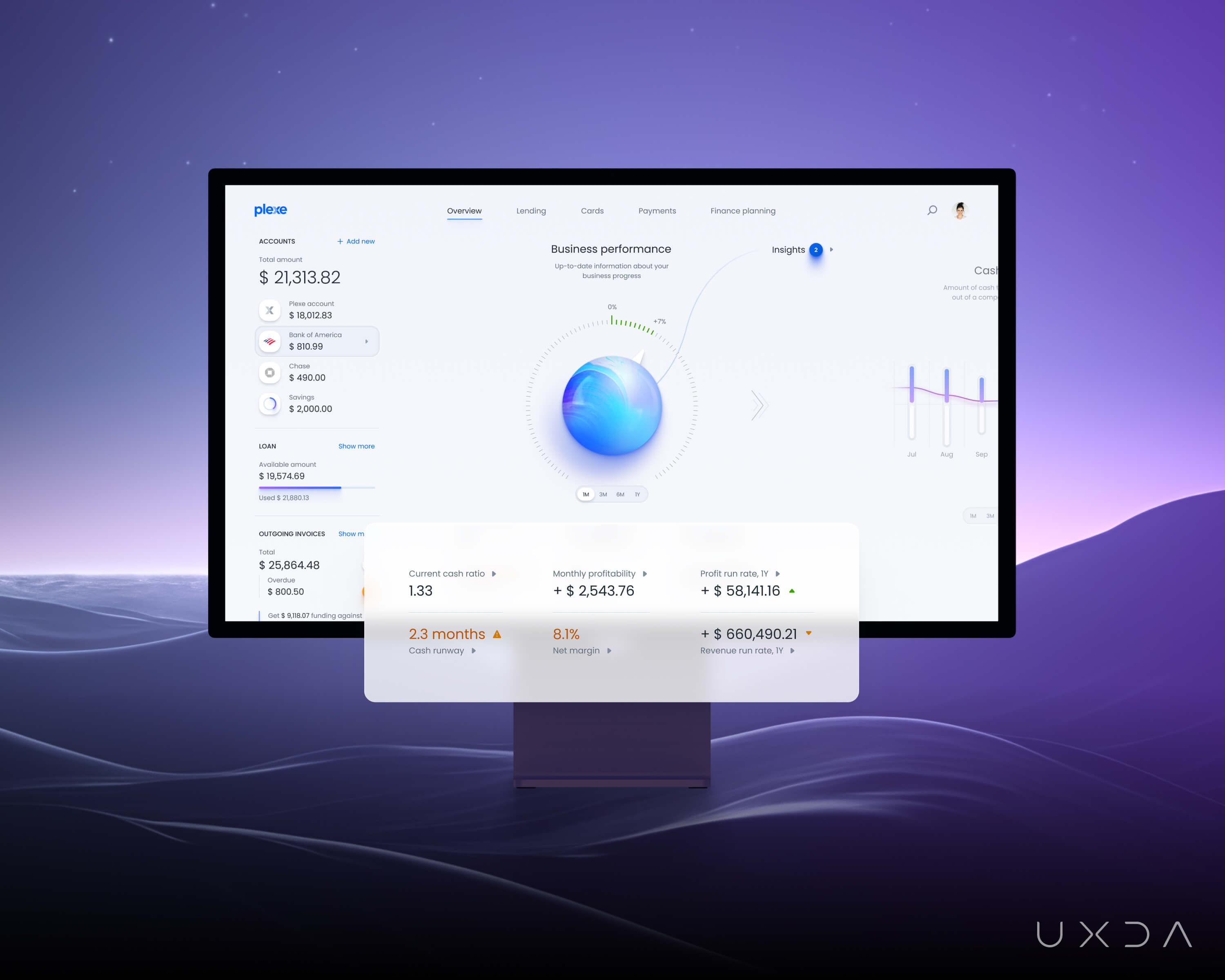

For example, at the heart of the SME banking platform's design we can put the AI-powered crystal indicator that consolidates crucial business information. It offers a sanctuary of control and a clear vision for future success. It goes beyond mere data, providing

insights and suggestions that not only illuminate the current state of affairs but also offer a roadmap for improvement.

Using data collected from different linked services and accounts, AI technology analyzes all aspects of the business and timely informs as to what to expect in the future and where to pay attention. Such SME banking platform will ensure that everyone, regardless

of financial knowledge level, can comprehend and steer their business toward prosperity.

The platform should process all cash flow and invoice data automatically, calculating available loan amounts based on the business performance and allowing users to view it at any time.

Acknowledging the difficulties SMEs encounter in sustaining consistent cash flow, the next-gen platform should provide users the flexibility to adapt lending repayment options to their specific needs, offering them more control over their financial commitments.

This flexibility caters to the unique circumstances of business owners, enabling them to opt for either a fixed amount or a percentage of their income.

Takeaway

The growing demand for financial guidance and management assistance among SMEs and self-employed individuals is undeniable. Business owners are actively looking for digital solutions that will meet their financial needs at the same level as retail banking.

Over the past decades, banks have gained a powerful asset that gives them an advantage in the market ─ trust from SMEs ─ but unfortunately the user experience has lagged behind. This is an ideal market window for Fintech companies. They are becoming active

players in the SME banking market with user-centric technologies. They bring together various services on one platform, providing greater convenience to SMEs' financial management.

A clear mission and flexible approach could allow SME banking platforms to significantly simplify the complexities of financial management and offer its clients a service that is easy and pleasant to use. Personalized notifications, insights, frictionless

digital experiences and responsive customer service are gaining customer satisfaction and loyalty.

The next generation of SME banking will be based on an analysis of customer expectations and a willingness to implement optimal customer service strategies. In addition, AI integration is a powerful extra for a competitive advantage today, but soon it will

become a mandatory requirement in the industry.

Check out my blog about financial and banking UX design >>